Business Valuation and Add-backs

Add-backs impact business valuation. Many business owners have a “number” in their head for what their business is worth. However, the raw EBITDA in the books may tell a different story.

Add-backs in small owner managed businesses can have a significant impact on the value and price a buyer is prepared to pay. This article examines how add-backs impact your business valuation.

Business valuation Add-backs & Normalised EBITDA

EBITDA stands for Earnings Before Interest, Tax, Depreciation, and Amortisation. It is a common standard earnings metric used in business valuations and when pricing transactions.*

Value is often expressed as a multiple of EBITDA.** For example, if a buyer offers a 3x multiple on a business generating $100,000 in EBITDA, the implied price is $300,000.

Normalised EBITDA refers to the add-backs, deductions and adjustments made to the bottom line to estimate the underlying operational earnings of the business. These normalisation adjustments feed directly into the valuation formula.

The Power of business valuation Add-backs

The maths is simple: as normalised EBITDA goes up, the business value goes up (assuming the multiple remains constant, which it may not!).

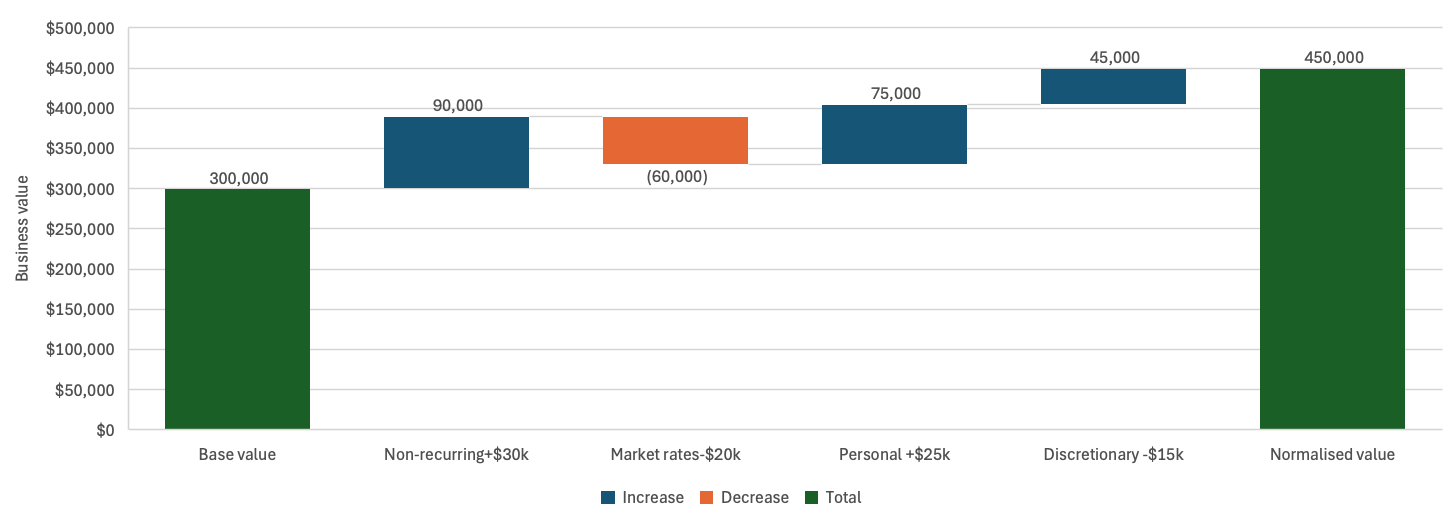

The figure below shows the power of normalising earnings. In the example, the add-backs result in an increase in EBITDA of $50,000, which increases the business value from $300,000 to $450,000.

Valuation bridge – the impact of normalisations on business value

A Critical Warning: Normalisation is a two-way street. While add-backs increase value, deductions decrease it. Furthermore, a savvy buyer will scrutinise how these adjustments impact expected future cash flows.

The four types of Add-backs

Add-backs, deductions and adjustments generally fall into four categories:

-

Non-recurring add backs (one-off events)

-

Items not at market rates (owner salary or rent)

-

Personal expense add backs (non-business related)

-

Discretionary expense add backs (optional spending)

1.Non-recurring add-backs

In financial reporting, non-recurring items are reported as significant and unusual expenses which are not expected to be repeated. Common examples include restructuring costs, legal settlements, and losses on asset disposals.

However, a buyer will want to understand the future expect impact of those non-recurring items:

-

AI & Automation: If you invested heavily in AI workflow automation this year, a buyer will want to know if this cost is truly “one-off” and how it improves future margins.

-

Redundancies: One-time redundancy costs should be added back, but the buyer will want to know if the reduction in staff will impact the business’s ability to service clients and maintain revenue.

2.Expenses Not at Market Rates

Expenses not at market rates are common in private, family-owned firms. The two “red flags” for valuers are:

- Underpaid/Overpaid Owners: The salary must be adjusted to what it would cost to hire a third-party replacement.

- Related-party Rent: If you pay rent to your own superannuation fund at a “friendly” rate, the valuer will use an external market rent report to normalise that expense.

The “Hidden” Deduction: If you are an owner taking a $50k salary but the market rate for your role is $150k, your normalised EBITDA will reduce by $100k. At a 3x multiple, this represents a $300,000 reduction in sale price.

3.Personal Add-backs

Personal Add-backs include costs not related to core operations, such as personal travel, club memberships, or motor vehicle costs.

These personal items are often “thorny” issues. Proving that they are genuinely personal can be difficult. Significant personal add-backs can signal poor record-keeping or “tax risk” to a buyer. Aggressive add-backs kill deals by eroding trust.

4.Discretionary Add-backs

Discretionary Add-backs are “optional” costs like charitable donations, staff retreats, or performance bonuses. While these are technically add-backs, the valuer or buyer will consider the consequences of removing them. For instance, if you eliminate staff bonuses to “boost” EBITDA, how will that impact future productivity and employee retention?

Summary: Understanding valuation Add-backs is Everything

Add-backs can have a significant impact on the value of a business. However, understanding those add-backs is key. An unsubstantiated add-back doesn’t just lower your price—it erodes buyer confidence.

* In business valuation practice multiples are used under the Market Approach. Metric multiples are observed for similar publicly listed companies or in transactions. When using comparable company and transactions, it is important to be consistent in the base metric. For example, the EBITDA for the comparables and the subject company need to be for the same period and normalised in the same way. Normalisation are also used under the Income Approach to estimate future expected cash flow to a business.

** EBITDA is often referred to as a proxy for cash. It’s not! Net profit after tax is a proxy for cash – tax and capital expenditure are real cash outflows! EBITDA is however a good measure for comparison. By removing depreciation and tax, this allows better comparison with firms that have different tax rates or depreciation policy.